Double Dipping Medicare

And Schizophrenic Government Health Care Regulation

This Post Includes A Readers Call To Action- Read To The End Please

Medicare Advantage seems to be the land of mischief where government provides a gravy train to big insurance. It likely isn’t a mistake that the Medicare Part C (Medicare Advantage) program’s birth coincides with negative Medicare budgets. My link to the CMS November 2024 financial report below takes you through this is detail. Medicare Advantage (Part C) came into existence as a pilot project when former President George W Bush’s administration created the Medicare (Part D) prescription insurance scheme.

This week the Wall Street Journal featured an article explaining that Uncle Sam paid twice for Veteran’s health services through payouts to Medicare Advantage and the Veteran Administration health care network. From the article, a prior December 2024 investigative piece found the federal government paid insurers an estimated $44 billion from 2018 through 2021 to cover veterans in Medicare Advantage plans who were also getting healthcare through the VA. I question why we have a VA system for Medicare aged Veterans (or any aged veteran for that matter)? Why not just put them in the Tricare health care system and be done with it? You get rid of the double dip immediately if that policy were voted in.

The Center for Medicare &Medicaid Services (CMS) November 2024 Financial Report

A document that is definite reinforcement for not taking a government job. I almost had myself committed trying to digest this monstrosity. 1.5-1.77 trillion dollars in 2024 was allocated for funding the Center for Medicare & Medicare Services. That is 22% of our total Government Budget! More by far than our defense budget. Up from 14% in 2023 of gov…

I have revealed in a prior post that the big insurance companies are double dipping using Medicare Advantage insurance chronic care management vehicles to dress up their rosters with sicker than reality beneficiaries and extra payment.

Then we learn that the Medicaid cuts proposed for the upcoming budget bill are being fought tooth and nail. One group fighting hard is the hospital lobby. This gripe also involves the old double dippity do. Using subsidized payment matching from Medicare, hospitals have created a money scheme whereby they volunteer a state Medicaid “health provider tax” in order to get 1-2 dollars from Medicare for each dollar they put into the state coffer. That is magical finance on all of us OR as a call for more debt.

Our local Lee Health system is counting on this mechanism to provide dollars lost from their leaving the public chartered sanctuary they enjoyed for 50 years. I recall they also are using the 340B drug pricing program and claiming “Lee Health System, Inc. DBA Lee Health is listed as a Disproportionate Share Hospital (DSH) in the 340B program database”. If you are the only hospital system in the market regardless of being rural or not, you get to claim you have a disproportionate patient population. Hospitals play the old “heart strings” musical and they keep getting more sympathy from the devil called government payment. Don’t fall for the argument that we can’t cut Medicaid as rural hospitals will fail. NEWSFLASH- NON RURAL SYSTEMS ARE GETTING RURAL HOSPITAL CARVE OUTS.

Our federal leadership keep falling for the safety net argument from Hospitals with fake price schedules and big insurance who incessantly demand policy forcing the last reluctant market participants into their control. In a nutshell that was the ruse played on America vis-a-vis OBAMACARE.

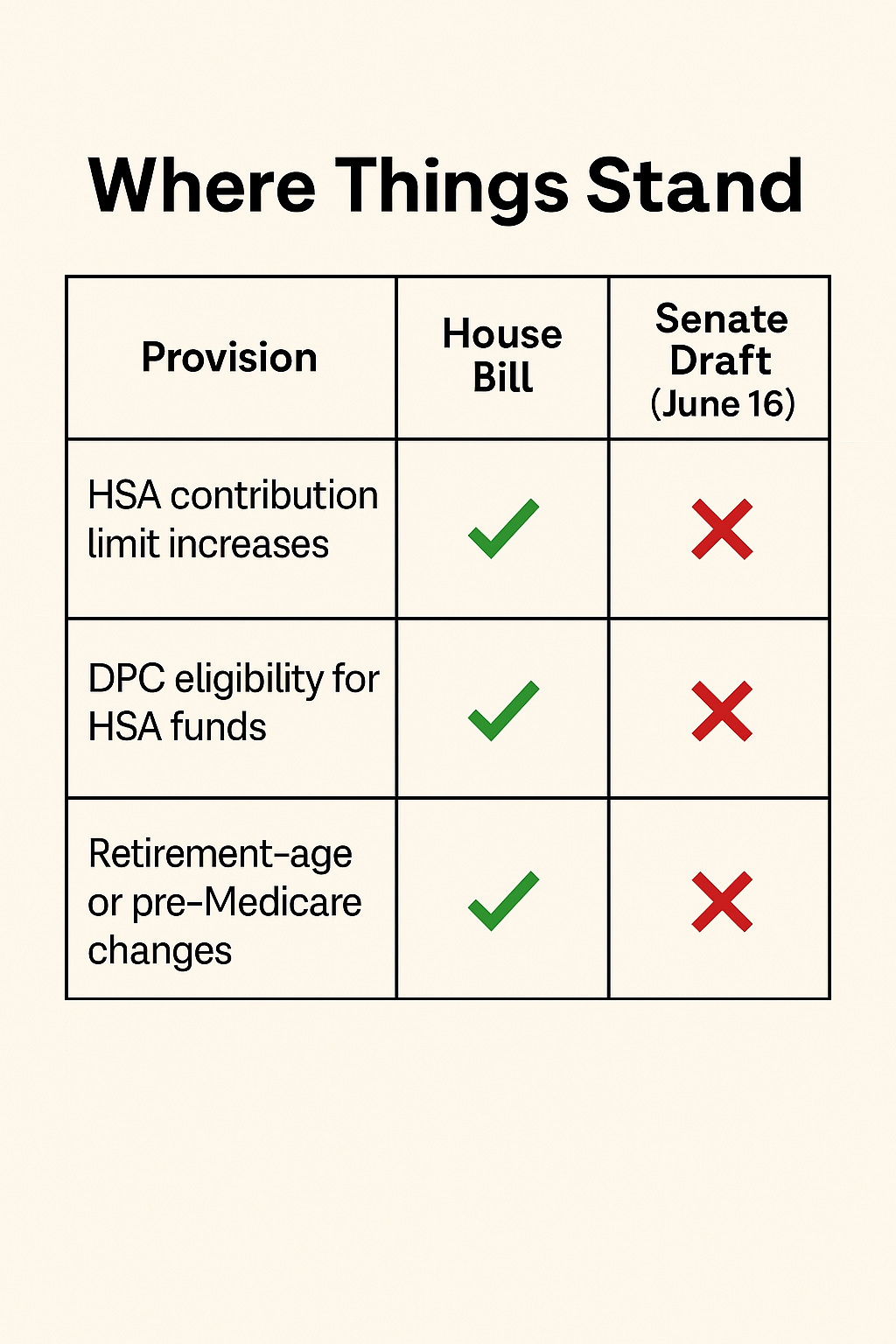

For Years Now Many Have Been Calling For Health Savings Account Expansion- Call To Action As The Senate Plans To CAVE AGAIN TO INSURANCE COMPANIES

The house of representatives had 10 provisions to expand the health savings account. The senate has pulled all of this.

Historically, Health Savings Accounts (HSA) were legislated into law for the Health Insurance Lobby. As patients’ experienced premium inflation with rising premiums at annual double digits, the market started to complain to big insurance.

Despite the price hikes, the insurance industry wanted to start off loading their risk by putting more out of pocket patient responsibility into their insurance products. The insurance companies excuse to buyers was people were consuming too much health care. They argued they needed to start putting cost disincentives into the consumption process.

To sell this cost transfer and in order to “ease” the individual’s up front access costs, they convinced government policy makers to allow a tax deduction for health care expenses. This sounded “sensible” BUT they also demanded this option can only be allowed for people who buy Preferred Network insurance policies. Uncle Sam has been doing Health Insurance’s bidding ever since I was a little boy.

I and many others who are seeking to unhinge government and insurance dependency to access healthcare have been arguing the irrationality of making buying insurance a requirement for incentives to save money for health care expenses,

Health Savings Accounts should be meant to let people shop wisely for care, free from insurance middlemen.

So why are they still shackled to only insurance-approved models?

You should be allowed to use your HSA for real care, not just to satisfy network contracts. Insurance status should have nothing to do with this “health care IRA”.

Enter Common Sense and The Direct Primary Care/Membership Model

All of our practice’s present patients understand that we are clearly providing health care at the level of comprehensive physician owned and operated traditional medical practice services and access. If this doesn’t qualify as a health care expense, I don’t know what would. The beauty of our practice model is involves comprehensive services at a fully transparent pricing for all to see and understand. People are buying our services and have been now for years. Dr. David Marconi MD and Michael Barry DO are geared up to help patients navigate the health care landscape AND on their journey for health and wellness.

Yet, apparently the senate wishes to buy the argument from the health insurance lobby that we are operating as an insurance product and thus patient’s can’t claim the dollars spent with us as eligible for health savings account treatment. Now that is irony. The Health Insurance lobby requires you buy their product IN ORDER TO HAVE AN HSA BUT ACTUAL HEALTH SERVICES CONSUMED IN A BUNDLED CARE PRACTICE AREN’T ALLOWED for HSA PAYMENT. If folks can’t see this as an openly hostile posture towards physicians and our involvement in health care, I am at a total loss to explain reality any further.

When we look at lobby dollars this situation stinks of “bought and paid for” policy.

The insurance lobby spent tens of millions influencing this bill.

They don’t want patients escaping their overpriced networks or doctors opting out of their fee schedules.

The Senate’s decision wasn’t a budget choice—it was a protection racket.

According to OpenSecrets, in 2025 the insurance industry spent nearly $50 million on lobbying, with major players including opensecrets.org+1opensecrets.org+1:

Blue Cross/Blue Shield – $6.5 million

America’s Health Insurance Plans (AHIP) – $4.83 million

Cigna – $3.46 million

Followed by AFLAC, Allianz, AIG, Prudential, Oscar Health, Allstate, State Farm, and others opensecrets.org+1opensecrets.org+1.

In the 2023–24 cycle, insurance PACs gave $24.6 million to federal candidates—$13.8 million to Democrats and $10.7 million to Republicans overall opensecrets.org+1healthcareuncovered.substack.com+1.

Top PAC donors included:

Council of Insurance Agents & Brokers – $2.16 million

New York Life – $1.43 million

Independent Insurance Agents & Brokers of America – $1.39 million

AFLAC – $1.34 million

NAIFA – $1.32 million

American Council of Life Insurers – $897k

This Bill Isn’t Final. But It’s Close.

The reconciliation bill is heading for debate and possible amendment before July 4.

Now is the moment to push the Senate to restore HSA eligibility for DPC.

If you're sick of seeing common-sense healthcare solutions blocked by insurance cronies in DC, now's the time to act.

Download my letter and send it to the Senate Finance Committee as well as any influential legislator involved with this particular portion of the budget bill. You can modify the letter to direct it to a member of the house. Feel free to place your personal reasons or experiences especially regarding the value of and desire for the Direct Primary Care model.

Tell Congress to bring DPC and HSA flexibility back into the bill—before it’s too late.” Final fate is uncertain: It hinges on committee action, floor debate, and confidence in passing a conference with the House before July 4.

This is a bipartisan issue and honestly, HSA’s should be available to any tax-paying US citizen. It shouldn’t be attached to any purchase requirement but rather an equal financial incentive to help people an off ramp from government dependency and control to free market access to health care, regardless of “class status”. If Medicare and Medicaid is going to subsidize a safety net class their funds should be agnostic to the provider offering real health care services.

Oh my…..there’s just SO much here to address. Doc you are 100 percent spot on. I’m going to have to compose my response on laptop as I have much to say, based on 45 years of aggravation, personal life experience, job experiences and now as a Medi(care?!?) member. It’s all such a horribly flawed system and even worse, most don’t see it and apparently just don’t want to, as they play along into the pocketbooks of insurers and big pharma who couldn’t care less about we the people or our health. It’s simply exhausting. Thank you for your forthright exposure and for being one of the medical minority who truly stands by their noble aspirations and oath to do no harm. More later…